Portugal is keeping the 100% mortgage guarantee for under-35s, whatever the IMF says

The IMF and the Bank of Portugal want the state guarantee that funds 100% of a first home for under-35s scrapped. The government says no, and blames the housing shortage for rising prices.

Portugal’s government will not touch the public guarantee that lets under-35s buy a first home with no deposit — and it said so after the International Monetary Fund argued the scheme should end and the Bank of Portugal warned it is inflating risk on bank balance sheets. Two of the loudest warnings a government can get about housing, and the answer was no.

How does Portugal’s public mortgage guarantee work?

The state stands as guarantor. Instead of the buyer scraping together the 10% or 20% deposit a bank normally wants, the state backs that slice and the bank lends up to 100% of the purchase. We’ve written the step-by-step guide to using the scheme, including the deadlines and the price caps.

By March, roughly 32,300 contracts had been signed under the regime, worth about €6.5 billion. This is not a niche measure — it now accounts for a very large share of young-buyer mortgage lending in Portugal.

Why does the IMF want the guarantee scrapped?

The Fund’s argument is Economics 101: if everyone can suddenly buy but the number of houses doesn’t change, what goes up is the price, not the number of owners. The IMF wants the guarantee curbed along with the IMT stamp-duty exemptions for young buyers, arguing both widened the imbalances in a market that was already stretched thin.

The Bank of Portugal gets to the same place by a different road. A 100% loan is by definition a loan with no cushion: if prices fall, the debt outlives the value of the house. The supervisor has flagged financial-stability risk and tightened lending rules, capping debt-service ratios while stretching repayment terms — the warnings and statements are all on the Bank of Portugal’s site.

What is the government’s answer?

That the problem isn’t demand, it’s supply. The ministry stresses that the state guarantee neither replaces nor waives the risk assessment banks are still required to run, and insists the shortage of homes is the determining cause of rising prices — not the public backstop. Along the way it promised another €750 million for the scheme’s envelope.

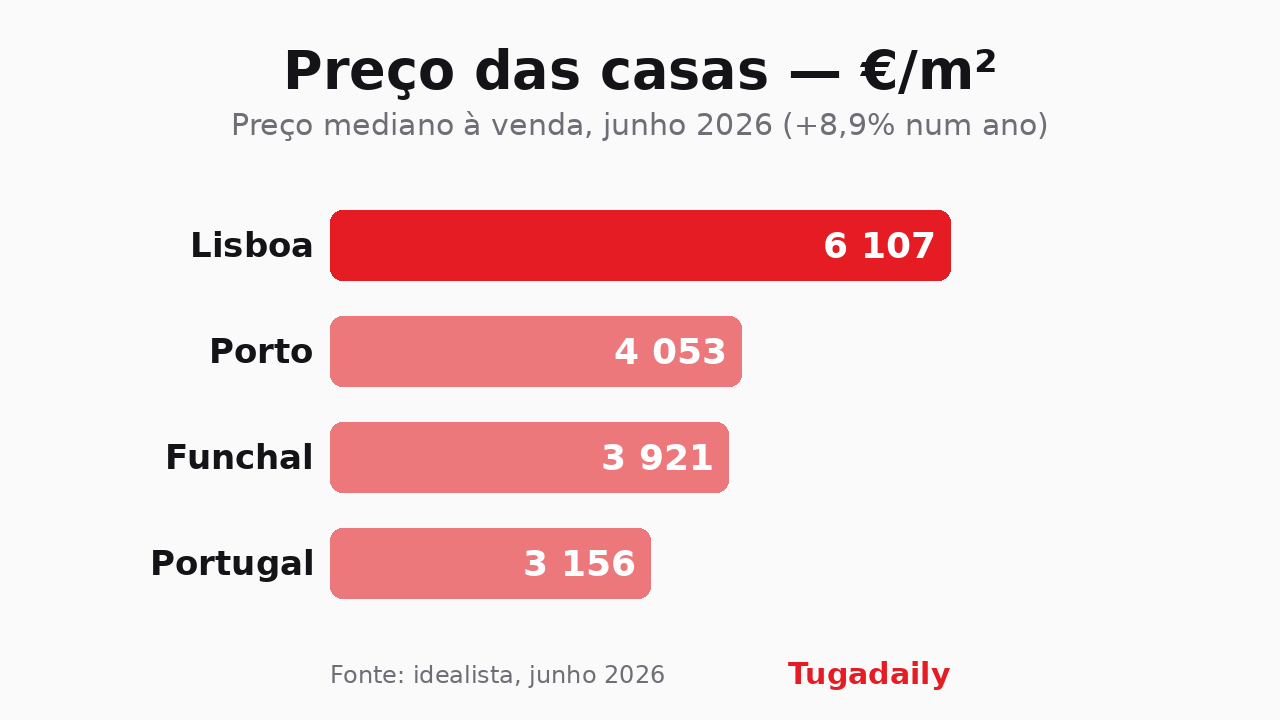

Both sides are partly right, which is what makes this hard. Portugal builds too little, licenses too slowly, and has a whole generation stuck renting — supply really is the hole in the boat. But until that hole is patched, handing more buying power to people bidding for the same houses pushes prices exactly the way we watch them move every month in our house price tracker.

In the end it’s a political bet with a date on it: the government is betting supply arrives before the bill does.

Image: Krzysztof Golik / Wikimedia Commons (CC BY-SA 4.0)